I used to be bullish on semiconductor designer and manufacturer Intel (INTC), but following the board’s decision to remove the CEO, I’m left uncertain about the company’s future. Instead, semiconductor designer AMD (AMD) is firing on all cylinders, with robust management and a fortified market position. As a result, I’m bullish on AMD and think it can generate a reliable 60% or more total price return in the next 24 months.

Pat Gelsinger, the CEO of Intel, was ousted from his position on December 1, 2024, causing a downgrade in my rating for its stock from a Buy to a Hold. The board lost confidence in his ambitious and costly turnaround strategy, much of which depended on developing a robust advanced semiconductor manufacturing division called Intel Foundry Services. This vital direction was meant to help the West protect itself from the concentrated advanced chip manufacturing operations in Taiwan, which is close to authoritarian China.

However, the board concluded that his plans were not delivering results quickly enough to address Intel’s financial struggles and competitive pressures. Indeed, during Gelsinger’s tenure, Intel’s market value significantly declined, falling to less than 30 times that of Nvidia (NVDA), the world’s strongest chip designer. Another way of looking at it is that Intel stock dropped more than 60% under Gelsinger’s tenure.

Therefore, it’s understandable why the board was not pleased. However, tackling both advanced semiconductor manufacturing and competitive chip design was never going to be easy. Maybe management, led by Gelsinger, bit off more than it could chew, but a critical weakness in Western geopolitics remains. The world relies on Taiwan’s TSMC (TSM) for manufacturing 92% of advanced semiconductors.

Not only does Gelsinger’s ousting and the uncertainty of the direction the company will take next spell trouble for Intel investors, but it also leaves the U.S. and the West vulnerable in the long term if the company decides to scrap its foundry plans. Many investors, including myself, are hoping the company will sell Intel Foundry Services to an entity that can focus wholeheartedly on fortifying Western semiconductor manufacturing interests.

Previously, when I analyzed Intel, I considered it to offer a compelling 18-month value opportunity based on momentarily depressed sentiment. However, given that the board has now ousted the CEO (who had the most semiconductor experience of anyone in the company—the board has several members with no semiconductor experience), the near-term value thesis has become uncertain. As a result, I have downgraded my rating from a Buy to a Hold.

My valuation model for Intel currently shows a negative margin of safety of -1.04%, based on a 2026 revenue estimate of $59.5 billion, a 2026 EBITDA estimate of $16.36 billion, and an EV-to-EBITDA terminal multiple of 8.5 (which reflects increased sentiment as the company enters a profit-harvesting phase in the near future).

The result of my model shows a 2026 enterprise value of $139.05 billion and a present-day intrinsic enterprise value of $116.23 billion, compared to a current enterprise value of $117.45 billion. My intrinsic enterprise value is calculated using a discount rate of 9.4%, approximately equal to the company’s weighted average cost of capital.

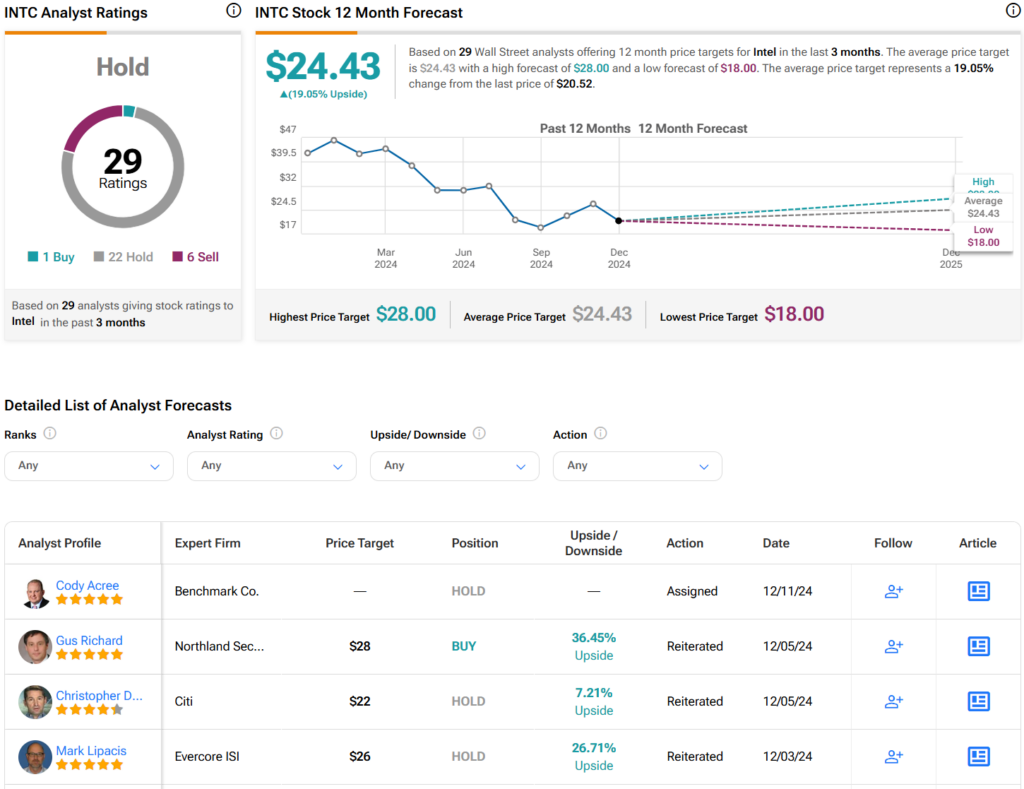

On Wall Street, Intel has a consensus Hold rating based on one Buy, 22 Holds, and six Sells. The average INTC price target of $24.43 per share indicates 19.05% upside potential over the next 12 months, reflecting that the near-term value thesis may remain intact. However, I am less convinced that the board and its new additions will be able to steer the ship to prosperity.

See more INTC analyst ratings

In contrast to Intel, AMD has demonstrated remarkable resilience, stability, growth, and market leadership in the semiconductor industry, leading me to be highly bullish on the company. It has consistently prioritized technological advancements across high-performance computing, AI chip development, and gaming and consumer electronics. AMD has delivered year-over-year EBITDA growth of 47.05% compared to just 8.76% for Intel.

AMD is experiencing high growth at the moment primarily due to its Data Center segment. In Q3 2024, Data Center revenue accounted for 52% of AMD’s total revenue, reflecting a 122% year-over-year increase. Management has forecast the company’s Q4 revenue to grow 22% year-over-year to $7.5 billion. Given these remarkable results that prove operational efficiency and organizational order, AMD is simply much more compelling than Intel to invest in based on objective data.

It’s worth considering that the semiconductor market is cyclical. Therefore, the major players like Nvidia and AMD are prone to a valuation collapse at some point in the next three to eight years, based on my analysis. This depends on how the demand from Big Tech companies for AI infrastructure evolves. Yet, at this time, there is no indication of a slowdown in the build-out of advanced data centers for AI. Therefore, I remain bullish on AMD for the foreseeable future.

By December 2026, AMD’s total revenue is likely to be approximately $40 billion, based on my analysis. If the company maintains an EV-to-sales ratio of approximately 8.5 (which is the midpoint of its current forward and trailing 12-month ratios), the company will have an enterprise value of $340 billion. Its current enterprise value is $204.99 billion, so an allocation today could render approximately a 65% total price return in two years based on my forecasts.

On Wall Street, AMD has a consensus Moderate Buy rating based on 22 Buys, eight Holds, and zero Sells. The average AMD price target of $184.33 per share implies 42.34% upside potential over the next 12 months, strongly supporting my independent analysis and personal Buy rating for the stock.

See more AMD analyst ratings

AMD is currently part of my growth portfolio strategy, and I have set a ‘take profit’ price target of $175, which I am likely to elevate as time progresses. I have considered investing in Intel previously, but given the current uncertainty, I prefer to allocate capital to robust management teams and fortified market positions. AMD offers this in spades, while Intel has shown repeated inconsistency that leaves its investment case currently fragile.

Dena Holloway is a writer, editor, and content creator based in the United States. She has written for a variety of publications, including Men With Wings Press, where she covers arts, automotive, travel, and fashion. She's also a certified yoga instructor and works as a freelance copywriter.