Uber (UBER) shares have had a rough ride in 2024, lagging behind the broader market with only a 12% gain over the last 12 months. However, my bullish outlook remains intact, considering that recent underperformance doesn’t reflect any weakness in the company’s business fundamentals. The company has been posting solid revenue and profit growth while generating impressive cash flow. The main factor weighing on investor sentiment seems to be the fear that robotaxis could disrupt the ride-sharing industry in the coming years.

While this is a valid concern, it arguably remains a distant risk. Uber has the capacity to adapt to emerging technologies, backed by its flexibility to make new investments, diversify its business, and maintain a financially viable ecosystem within the broader mobility industry.

In this article, I’ll share a few reasons why I believe Uber stock is worth considering as a Buy in 2025 and why the market seems to be overlooking them.

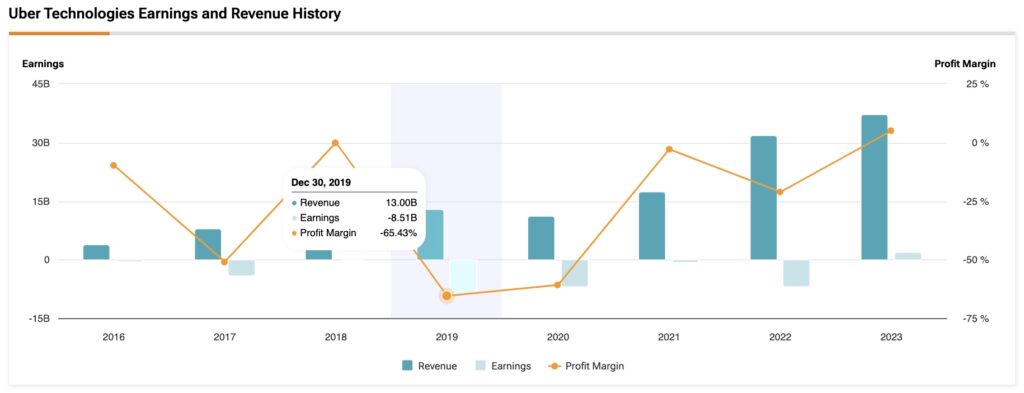

To start, one of the first reasons behind my bullishness on Uber lies in the value proposition of its ride-sharing and food delivery business. A look at Uber’s top-line evolution over the last few years shows that the company’s revenue was nearly $42 billion during the past twelve months, while in 2019, that figure was $13 billion.

Having quadrupled its revenues over the last five years, I wouldn’t be surprised if this growth trend continues, albeit not as robustly, but with a certain intensity. More and more individuals have realized the convenience of both ride-sharing and food delivery. One possible cause for this trend may also be connected to the increasing costs of owning a car in many parts of the world, favoring the use of ride-sharing, especially in large cities.

As a result, analysts estimate that Uber’s top line could grow by 17.3% in 2024, followed by 15.7% and 15.6% growth in 2025 and 2026, respectively. Moreover, with Uber set to report its second consecutive full year of profitability, projections suggest that its EPS CAGR over the next three to five years will be an impressive 41.2%. Therefore, considering that Uber is currently trading at a forward P/E ratio of 22.5x, if the long-term CAGR estimates prove accurate or close to it, Uber’s PEG ratio stands at 0.55, which appears very cheap.

Another piece of evidence that connects with my favorable outlook for Uber stock is that the company has been able to expand profit margins nicely in recent years as it has benefited from economies of scale. At the moment, operating margins of 6.4% are significantly higher than the negative 75% seen in 2020.

Much of this reversal in operating margins over the past few years correlates with Uber’s asset-light business model, where drivers use their own cars (which end up being Uber’s assets). Thus, the company is able to scale its operations without a proportional increase in capital expenditure. This approach allowed Uber to generate $1.7 billion in free cash flow in Q3 2024, up 133% from the same period last year.

Although the company’s balance sheet is not impeccable–the company holds $10.9 billion in long-term debt–it does hold about $9 billion in cash, equivalents, and short-term investments. This gives the company plenty of capital to fund growth initiatives. It also means that cash and investments will likely not be a bottleneck for Uber, and the company can use some of its growing cash flow to gradually pay down long-term debt, reduce interest expenses, and boost profitability.

The third point where I see Uber as a great Buy opportunity throughout 2025 correlates with the bearish momentum around its stock, shadowed by Tesla’s (TSLA) robotaxi fears, where I see a certain tone of exaggeration. As shown in the graph below, throughout 2024—particularly in the last quarter—there was a lot of hype around Tesla’s stock announcement, especially with its upcoming robotaxi project set for 2025. This created a lot of negative sentiment towards Uber’s business model.

In theory, fears are not unreasonable. Tesla’s CEO Elon Musk has said over the past year that the model for Robotaxi service would be a mix between Airbnb (ABNB) and Uber, where Tesla would own and operate a fleet of cars and sell to private individuals who want to own their own robotaxis. However, according to Wedbush four-star analyst Dan Ives, the reality of Robotaxi’s implementation is still a long way off. According to the analyst’s comments from earlier this year, “Our view is while this is an exciting announcement around robotaxis we do not expect full autonomy (no steering wheel models) until 2030.”

Another point in Uber’s favor is how much its business has diversified beyond just ride-sharing. The company has built a highly profitable ecosystem where food delivery, logistics, and transportation play key roles. In Q3, delivery alone accounted for 30% of Uber’s revenue, while freight made up 11%. Uber’s management team seems well-prepared to adapt to disruptive changes in the ride-sharing industry. Indeed, CEO Dara Khosrowshahi believes that Tesla’s robotaxi project will rely on resources Uber already has in order to be financially viable.

Looking at what Wall Street analysts are saying about Uber stock, the mood is pretty optimistic. Out of 35 experts, 33 are all in favor of buying, while just two are sitting on the fence. In addition, the average price target of $93.35 suggests that the stock is significantly undervalued, pointing to an impressive upside potential of 44.5% from its current price.

See more UBER analyst ratings

As highlighted throughout the article, there are numerous reasons to be bullish on Uber heading into 2025. The company’s fundamentals are the strongest they have ever been, growth is accelerating, and the outlook for the future is exceptionally bright. I see the stock as a prime example of “growth at a reasonable price,” especially since concerns over the Robotaxi project appear wildly overstated and are already baked into the stock’s valuation.

For these reasons, I’m maintaining my confident Buy rating on UBER.