Shopify (SHOP) and Block (SQ) are two very different companies, yet both operate in the e-commerce and payments sectors, serving businesses in related ways. Over the past five years, their trajectories have been quite similar – both were major beneficiaries of pandemic tailwinds, only to face significant drawdowns as those effects faded. Using TipRanks’ Stock Comparison Tool, this article provides a closer look at the recent developments of both companies, including their latest Q3 earnings reports, leading to a neutral outlook for Shopify and a bullish outlook for Block, which appears to be the better buy for now.

Now, let’s dive deeper into the comparison and explore the reasons behind my outlook for each company.

Before delving into the investment thesis for Shopify and Block, it’s important to first highlight their business models and target audiences.

Shopify is primarily an e-commerce platform that enables businesses to create and manage online stores. It offers tools for selling products, processing payments, and managing inventory. Its main focus is to help entrepreneurs and businesses of all sizes sell goods online easily.

Block, on the other hand, is a financial services and payments solutions company. It offers point-of-sale (POS) systems, payment processing, and other financial services, mainly targeting small to medium-sized businesses (SMBs) that need simple, user-friendly solutions for processing payments.

In terms of how they generate revenue, Shopify generates revenue through tiered subscription plans, starting at $39 per month, with additional fees for payment processing and extra features. Meanwhile, Block offers a free basic plan for payment processing, charging transaction fees (typically 2.6% + 10 cents for in-person payments), and paid services like payroll and advanced POS features. Additionally, Block has shifted some focus to cryptocurrency, emphasizing Bitcoin (BTC-USD) and decentralized financial services through its Cash App.

While I remain somewhat skeptical about Shopify for now, in contrast to my more optimistic outlook on Block, it is interesting to note that both companies have shown similar patterns over the past five years, experiencing significant drawdowns following the pandemic.

This can be attributed to the fact that both Shopify and Block (formerly Square) were trading at high valuations heading into 2021, fueled by pandemic-driven growth, low interest rates, and the booms in e-commerce and fintech. As investors anticipated continued hyper-growth, both stocks saw sharp price increases.

However, after the pandemic surge, Shopify faced a slowdown in merchant base growth, raising concerns about its ability to retain customers, especially as competition intensified. On the other hand, Block experienced significant volatility in its Bitcoin-related revenue through Cash App, making its earnings more unpredictable and more exposed to market cycles and crypto price fluctuations. These factors contributed to major drawdowns for both stocks, with Shopify falling 82% and Block dropping 85%.

Although I have a neutral outlook on Shopify, this stance is not a reflection of the company’s fundamentals. Shopify’s investment thesis is supported by its impressive growth trajectory in recent quarters, particularly its ability to sustain strong revenue growth while expanding profitability margins.

Over the past three years, Shopify’s revenue has grown at a CAGR (compound annual growth rate) of 25%, while maintaining gross margins of 51%. Looking ahead, the company is expected to grow EPS at an impressive 43.6% annually over the next three to five years. However, my main concern lies in valuations. With a forward P/E ratio of 88.8x, Shopify trades at a relatively high multiple, resulting in a PEG ratio of 2x, which suggests the stock is somewhat richly valued.

These stretched valuation multiples reflect Shopify’s strong momentum, further supported by its Q3 2024 earnings, reported on November 12, which helped boost Shopify’s stock by more than 25%. The company posted 26% year-over-year revenue growth, reaching $2.16 billion and marking the sixth consecutive quarter of growth above 25%.

Noteworthy, this growth is not only in the top line but also in operational efficiency and profitability. A standout achievement in Q3 was Shopify’s ability to drive strong revenue growth while simultaneously expanding profit margins, a rare feat among high-growth tech companies. Operating income surged 132% from $122 million in Q3 2023 to $283 million in Q3 2024, driven by scaling operations rather than cost-cutting. As a result, operating expenses grew by just 7% year-over-year, while gross profit increased by 24%, showcasing Shopify’s ability to scale efficiently.

In comparison, Block has shown strong performance similar to Shopify, with a 52% increase in the stock price over the past year. I maintain a slightly more bullish view of the company despite its slower growth profile and lower margins (36% gross margin) compared to Shopify. Over the past three years, Block has grown its revenue at a CAGR of 12.5%, which is respectable but not exceptional for a growth stock.

Given this more modest growth trajectory, Block currently trades at a forward P/E ratio of 24.2x, nearly double the industry average. However, the company is forecasting robust bottom-line growth, with an expected CAGR of 39.9% over the next three to five years, which gives Block a PEG ratio of just 0.6x, suggesting the stock is undervalued relative to its growth potential.

Even though the current momentum for Block is highly bullish, its Q3 results, reported on November 7, were mixed: the company met bottom-line expectations but missed revenue estimates, despite posting 6% revenue growth. However, investors seemed to focus more on profitability, as Block made notable progress in gross profit growth. Total consolidated gross profit reached $2.25 billion, reflecting a 19% year-over-year increase.

What stood out in Block’s earnings report was the strong momentum in its Cash App segment, which saw 21% year-over-year growth in gross profit, outperforming the Square segment, which delivered a 16% rise in its gross profit. Cash App now represents 58% of Block’s total gross profit, highlighting its crucial role in driving the company’s overall growth.

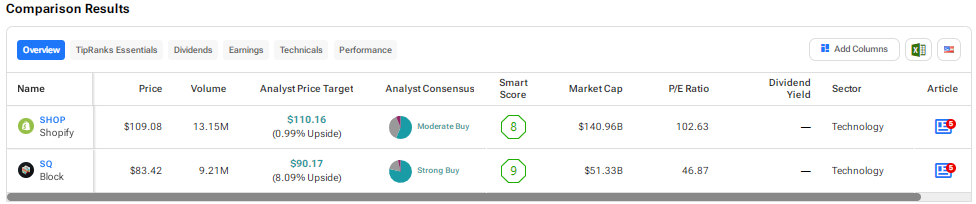

Looking at the Wall Street consensus, Shopify stock is rated a Moderate Buy, with 11 out of 18 analysts bullish, six having a Hold rating, and only one analyst assigning a Sell recommendation. The average SHOP stock price target of $85.31 suggests a downside potential of about 22%, highlighting concerns about the company’s valuations.

See more SHOP analyst ratings

On the other hand, Block stock is rated a Strong Buy based on 22 Buys, four Holds, and one Sell recommendation. The average SQ stock price target is $89.50, implying 7.3% upside potential.

See more SQ analyst ratings

While both Shopify and Block have been standout performers this year, with strong progress in recent quarters, especially in Q3, Block appears to be the better investment right now.

Shopify offers greater growth potential and stronger margins, but this comes with a much higher valuation, which I believe is justified by its premium growth prospects. In contrast, Block has a more modest growth trajectory, yet it is steadily progressing toward profitability, driven largely by the momentum in its Cash App business. Moreover, Block trades at valuations that seem undervalued relative to its strong EPS growth forecast, making it a less risky investment in my view.

Dena Holloway is a writer, editor, and content creator based in the United States. She has written for a variety of publications, including Men With Wings Press, where she covers arts, automotive, travel, and fashion. She's also a certified yoga instructor and works as a freelance copywriter.