High-yield dividend stocks can be a powerful way to generate steady income – and a few are offering payouts that crush the market average.

Investment firms Jefferies and BTIG have recently pointed to two such names that stand out. Both offer dividend yields approaching 10% – about seven times higher than the S&P 500 average.

However, diving into high-yield stocks calls for extra diligence. While they can offer attractive income, they may also come with increased risks, such as potential dividend cuts or underlying business challenges.

That’s why we turned to the TipRanks database to see whether the rest of Wall Street is backing these picks. Here’s what we found.

Blue Owl Capital Corporation (OBDC)

We’re starting with a BDC – short for Business Development Company. These companies step in where traditional banks often won’t, offering capital and credit to growing businesses that power the U.S. economy. Blue Owl Capital Corporation (OBDC) is a key player here, providing financing and credit services to the kinds of firms that have long served as the country’s economic engine.

OBDC is managed by Blue Owl Credit Advisors, an arm of Blue Owl Capital Inc., and it specializes in financing middle-market companies. The firm takes a debt-first approach, with a selective eye toward equity, building a portfolio that now spans 236 businesses with a combined fair value of $17.7 billion. The average investment size is $75 million.

Looking at the drill-downs, we find that the company’s portfolio is made up mainly of first-lien senior secured loans, at ~76% of the total. Common equity makes up ~12%, and second-lien senior secured loans make up ~5%. Of the total portfolio, 96.5% of the assets are floating rate, and the remainder are fixed. OBDC invests in a wide range of business sectors, and more than half of its investments are in the Southern and Western regions of the US.

Financially, the company reported adjusted net investment income of $0.39 per share in Q1 2025. That came in below expectations, missing forecasts by 4 cents.

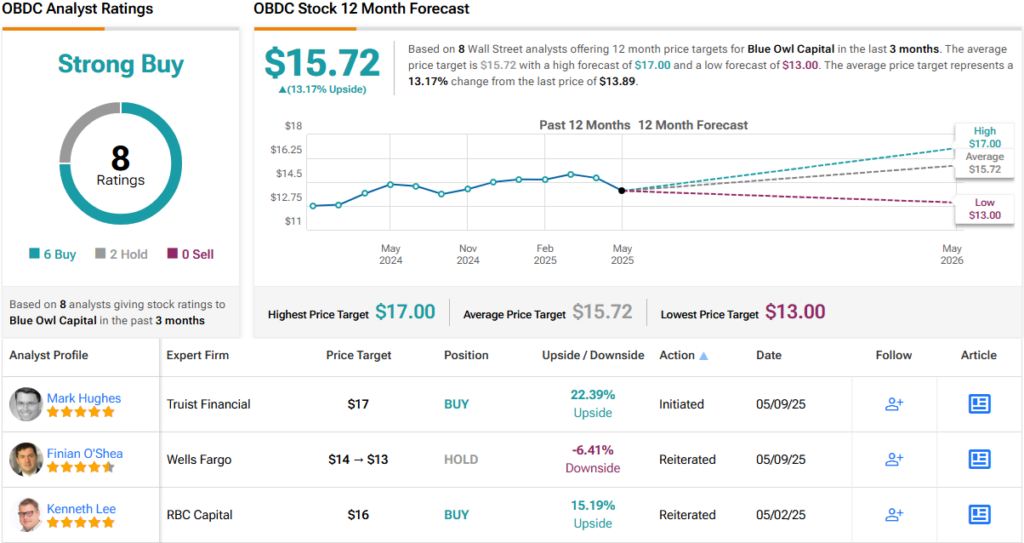

The regular dividend was declared at 37 cents per share, and was accompanied by a supplemental payment of 1 cent per share. The regular dividend annualizes to $1.48 per share and gives a forward yield of 10.7%.

Jefferies analyst Matthew Hurwit covers this BDC, and he is impressed by the company’s potential to deliver returns.

“We view OBDC as a compelling income investment with a base-case total return driven by a double-digit dividend yield and modest NAV/share growth. In an upside scenario, continued strong credit performance and increased investor recognition could result in multiple expansion (price/NAV moving to a premium), delivering additional capital gains. In a downside scenario, a material economic downturn could pressure portfolio companies and valuations; however, OBDC’s conservative portfolio (83% senior secured loans) and low non-accruals should help mitigate losses. Overall, OBDC’s large scale, prudent underwriting, and support from Blue Owl’s platform underpin a favorable risk-adjusted return profile for income-focused investors,” Hurwit opined.

Hurwit goes on to put a Buy rating on OBDC shares, and his $16 price target implies a one-year upside potential of 15%. Add in the regular dividend yield, and this stock’s total one-year return may reach as high as 25.7%.

Overall, OBDC has a Strong Buy consensus rating from the Street’s analysts, based on 8 recent reviews that include 6 Buys and 2 Holds. The shares are priced at $13.89, and their $15.72 average price target implies 13% upside potential. (See OBDC stock forecast)

Apollo Commercial Real Estate (ARI)

Next up is a REIT, or real estate investment trust. These companies are well-known as dividend champs; dividend payments make a convenient vehicle for compliance with tax regulations to return profits directly to shareholders. Apollo Commercial Real Estate operates in the US and Europe, where it both originates and invests in commercial real estate-related debt investments, including senior mortgages and mezzanine loans. The company’s portfolio is collateralized by properties, and as of this past March 31, it had an amortized cost of $7.7 billion.

Apollo Commercial Real Estate is externally managed by an indirect subsidiary of the alternative investment manager, Apollo Global Management. The larger global asset manager has invested more than $105 billion into commercial real estate since 2009, and $26 billion of that total was invested on behalf of Apollo Commercial Real Estate. Apollo Commercial Real Estate uses its relationship with the larger asset manager to realize advantages in its business, in sourcing, evaluating, underwriting, and managing its investments in commercial real estate.

Apollo Commercial Real Estate’s portfolio contains 48 loans, primarily floating-rate and mortgage loans. The weighted average remaining term of the loans is 2.4 years. The portfolio is diverse, with 24% in office space, another 24% in residential properties, and 21% in hotels. Of the remainder, 12% is in retail properties. Geographically, 32% of the portfolio is in the UK and 20% is in New York. The next largest geographic segments of the portfolio are Europe, at 17%, and the American Southeast, at 11%.

On the financial side, Apollo Commercial Real Estate last reported results for 1Q25. In that quarter, the company realized a net income attributable to common shareholders of 16 cents per share. The company’s distributable earnings per diluted share came to 24 cents. On April 15, the company paid out a common share dividend of 25 cents; the annualized rate of $1 per common share gives a forward yield of 10.4%.

This stock has caught the eye of BTIG analyst Tom Catherwood, who notes that the company is agile, and capable of shifting its portfolio stance to meet changing conditions.

“While we have been positive on ARI’s platform for some time, we feared that large-scale challenged loans (namely Steinway Tower and a portfolio of hospitals in MA) could require the company to retain additional capital, limiting its ability to consistently originate and grow its loan book. That said, ARI swiftly resolved its MA hospital loan exposure, and given recent sales activity at Steinway, we expect the company to start collecting income on its $288M senior mezz loan on the property in 2Q25. Given a healthier position in Steinway, steady loan origination pipeline, institutional backing from Apollo Global Management, and platform in the UK/Europe (52% of the loan book), we believe ARI is positioned to outperform its peer group during a time of volatility for the US commercial real estate market,” Catherwood explained.

Catherwood’s comments support his Buy rating on ARI shares, while his $11 price target suggests that ARI will gain 14.70% going forward. With the dividend yield, this stock’s total return may reach 16%. (To watch Catherwood’s track record, click here)

That’s one side of the Street. The broader analyst consensus takes a more cautious stance, landing at Hold (i.e., Neutral). Out of 6 recent ratings, there are 2 Buys, 3 Holds, and 1 Sell. With shares trading at $9.59 and an average price target of $9.80, that points to a more muted upside of 2% over the next year. (See ARI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.