Two of this year’s hottest stocks are both darlings of the artificial intelligence (AI) movement. Data analytics software developer Palantir Technologies(NASDAQ: PLTR) and cybersecurity specialist CrowdStrike(NASDAQ: CRWD) have been in the spotlight for much of 2024 — albeit for much different reasons.

While Palantir has finally proven that it is a rising star in the enterprise software arena, CrowdStrike’s reputation took a major blow earlier this year after a glitch in its platform caused unprecedented outages for many of its customers.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Nevertheless, I remain bullish on CrowdStrike’s long-term narrative — so much so that I think the company could be worth more than Palantir by the next decade.

Below, I’m going to illustrate Palantir’s rapid ascent to the top of the AI software realm and break down how CrowdStrike could emerge as the more valuable company in the long run.

At the time of this writing, Palantir stock has gained 287% in 2024 and is the second-best performing stock in the S&P 500.

The primary driver behind Palantir’s surge is immense demand for its Artificial Intelligence Platform (AIP) software. Until the release of AIP, Palantir was widely regarded by skeptics as a consulting operation for the federal government with limited software capabilities. But over the last year, Palantir has flipped that narrative right on its head.

Over the last 12 months, Palantir has increased its customer count by 39%. Yet more impressively, the company has swiftly penetrated the private sector, growing its commercial customer count by over 50% for the trailing-12-month period ended Sept. 30.

The obvious benefit of increased customer counts is accelerated revenue. But what makes an investment in Palantir even more special is the company’s ability to expand margins and begin generating positive free cash flow and net income in tandem with rising revenue.

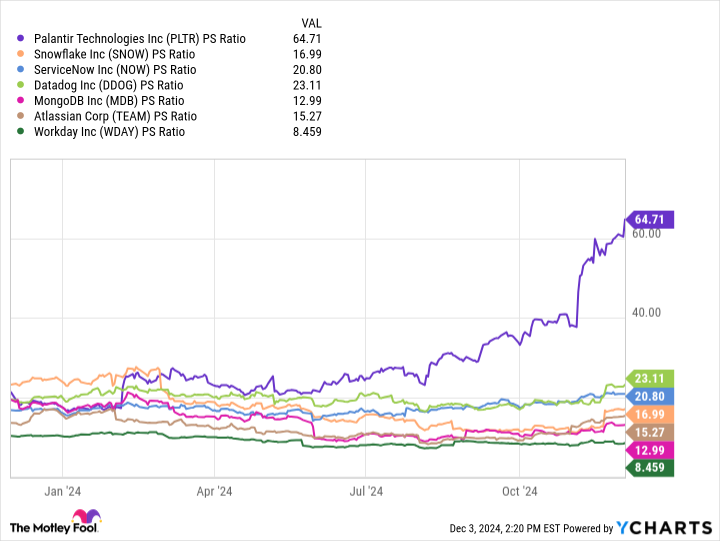

All of these factors make Palantir look like a no-brainer investment opportunity… that is, until you take a look at the chart below.

PLTR PS Ratio data by YCharts

The clear outlier in the chart above is that Palantir’s price-to-sales (P/S) ratio of 65 is not only the highest among this cohort, but is nearly triple the next closest comparable business. While it can be argued that Palantir deserves a premium multiple, the stock has experienced outsize valuation expansion during an otherwise short time period. Candidly, I think it’s this very dynamic that is causing some hedge funds to materially trim their exposure to Palantir and take profits.

Image source: Getty Images.

I’ll get the obvious point out of the way up front: CrowdStrike is by no means a cheap stock. Even with the material sell-off that was driven by the security outage over the summer, the stock still trades at a meaningful premium above its peers.

CRWD PS Ratio data by YCharts

Nevertheless, I see some key differences between an investment in CrowdStrike and one in Palantir.

As I previously explored, CrowdStrike was in rare company a few years ago during the height of the COVID-19 pandemic. In fact, demand for CrowdStrike’s products actually rose during the COVID-19 recession. I see two reasons for this. The obvious reason is that work-from-home protocols became the norm during peak pandemic days. As such, businesses needed to double down on cybersecurity protocols on work-issued devices during this phase of remote work.

However, taking this a step further, I’d argue that CrowdStrike is positioned well during just about any economic cycle because investment in cybersecurity is increasingly becoming a non-negotiable.

In other words, while data analytics is important, Palantir’s value proposition becomes harder to justify during tough times when budgets are tight. In my eyes, the same cannot be said for cybersecurity.

CrowdStrike’s security outage incident occurred on July 19. About a month later, the company reported earnings for its second quarter of fiscal 2025 (ended July 31). To me, the most important figure in that report was annual recurring revenue (ARR), which clocked in at $3.9 billion.

Fast forward to Q3, when CrowdStrike ended the quarter with just over $4 billion in ARR.

Despite any reputational damage from the outage, CrowdStrike has still managed to grow its ARR over the last two quarters. I think this is a testament of the company’s superior products, and the heavy reliance its customers have on CrowdStrike’s security backbone.

At the end of the day, I think both Palantir and CrowdStrike are pricey stocks. However, Palantir’s valuation is stretched and the stock is overbought. As such, the company has to prove that it can grow into this premium valuation — which will be no easy feat given how intense the enterprise software landscape is. Over time, it could become more challenging to compete with existing software providers even if Palantir does have the superior product. Palantir’s ability to scale in the long run could all boil down to pricing compared to competing platforms.

By contrast, I think businesses are going to continue increasing investment in cybersecurity as threats of fraud and ransomware rise and become more sophisticated. Given CrowdStrike’s proven ability to grow during difficult economic times such as recessions as well as challenging business-specific periods (i.e. the outage), I think the company is positioned to accelerate sales, expand margins, and compound profits over the next several years.

For these reasons, I think CrowdStrike has a better chance of experiencing an expanded valuation from current levels and could surpass that of Palantir should the software developer show any sign of protracted growth.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $369,349!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $45,990!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $504,097!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of December 2, 2024

Adam Spatacco has positions in Palantir Technologies. The Motley Fool has positions in and recommends Atlassian, CrowdStrike, Datadog, Fortinet, MongoDB, Okta, Palantir Technologies, ServiceNow, Snowflake, Workday, and Zscaler. The Motley Fool recommends Palo Alto Networks. The Motley Fool has a disclosure policy.

Prediction: This Spectacular Artificial Intelligence (AI) Stock Will Be Worth More Than Palantir by 2030 was originally published by The Motley Fool

Dena Holloway is a writer, editor, and content creator based in the United States. She has written for a variety of publications, including Men With Wings Press, where she covers arts, automotive, travel, and fashion. She's also a certified yoga instructor and works as a freelance copywriter.