Artificial intelligence (AI) has helped Nvidia‘s (NASDAQ: NVDA) stock clock stellar gains in 2024, with shares of the semiconductor giant rising more than 183% as of this writing, but it seems that investors are now having doubts about the company’s ability to maintain its stunning growth rate over the long run.

This is probably why Nvidia stock has retreated despite delivering better-than-expected numbers and guidance last month. The company’s revenue for the third quarter of fiscal 2025 increased an impressive 94% from the year-ago period to $35.1 billion, while earnings jumped 103% year over year to $0.81 per share.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

However, Nvidia’s revenue guidance of $37.5 billion for the current quarter suggests that its top line is on track to increase at a relatively slower pace of 70% from the year-ago quarter. Additionally, the margin pressure that the company will face in the near term on account of the rollout of its Blackwell processors seems to have dented investors’ confidence.

Of course, Nvidia can overcome these challenges and deliver more gains to investors. However, those who missed out on Nvidia’s rally and are looking for a relatively cheaper AI stock that isn’t trading at an expensive 31 times sales can consider taking a closer look at Marvell Technology(NASDAQ: MRVL). Let’s look at the reasons why.

Marvell Technology released its fiscal 2025 third-quarter results (for the three months ended Nov. 2) on Dec. 3. The chipmaker’s total revenue increased 7% year over year to $1.52 billion, which was higher than the consensus expectation of $1.46 billion. Its non-GAAP (adjusted) earnings increased to $0.43 per share from $0.41 per share in the year-ago period, again beating the consensus estimate of $0.41.

You might be wondering why Marvell may be a good alternative to Nvidia considering its slow pace of growth, but a closer look at the company’s data center business will reveal the true picture. The data center segment produced 73% of Marvell’s top line last quarter, up from 39% in the year-ago period. The segment’s revenue nearly doubled on a year-over-year basis to $1.1 billion, offsetting the steep declines that the company witnessed in other segments such as enterprise networking, carrier infrastructure, automotive/industrial, and consumer.

The good part is that the strength of Marvell’s data center business, which is benefiting from the growing demand for custom AI processors and optical networking equipment, will be enough to lift the company’s growth higher in the current quarter. That’s evident from Marvell’s fiscal fourth-quarter revenue guidance of $1.8 billion, which would be a 26% jump from the year-ago period. Analysts would have settled for $1.65 billion in revenue from Marvell for the current quarter.

Additionally, the chipmaker expects earnings to land at $0.59 per share in the current quarter, which would translate into a 28% increase from the same period last year. Marvell CEO Matt Murphy pointed out on the latest earnings conference call that the stronger-than-expected demand for its custom AI processors played a central role in its better-than-expected performance and robust guidance.

Marvell management believes that it will “significantly exceed the full year AI revenue target of $1.5 billion.” The chipmaker is forecasting $2.5 billion in AI chip sales in the next fiscal year, though analysts believe that its AI-focused revenue could go up to $3 billion next year.

It is easy to see why analysts are expecting the strong growth in Marvell’s AI-related business to continue. After all, the company is one of the two major designers of custom chips, which are being developed by major cloud computing providers to reduce their reliance on Nvidia by developing in-house chips. These cloud companies turn to the likes of Marvell and Broadcom for designing their in-house chips.

Reuters reports that the market for custom AI chips could be worth an impressive $45 billion by 2028, compared to an estimated $10 billion this year. Meanwhile, the company sees an additional revenue opportunity of $26 billion in data center switching and interconnect by 2028, thanks to AI. So, it won’t be surprising to see Marvell delivering much stronger revenue and earnings growth in the next fiscal year and beyond.

Based on Marvell’s fiscal Q4 guidance, the company is on track to finish fiscal 2025 with revenue of $5.75 billion. That would be an increase of just 4% from fiscal 2024 levels. Its earnings are on track to hit $1.56 per share for the full year, an increase of 3% over the previous fiscal year.

Analysts, however, are expecting much stronger growth in fiscal 2026 (which will begin in February next year and coincide with 11 months of calendar 2025).

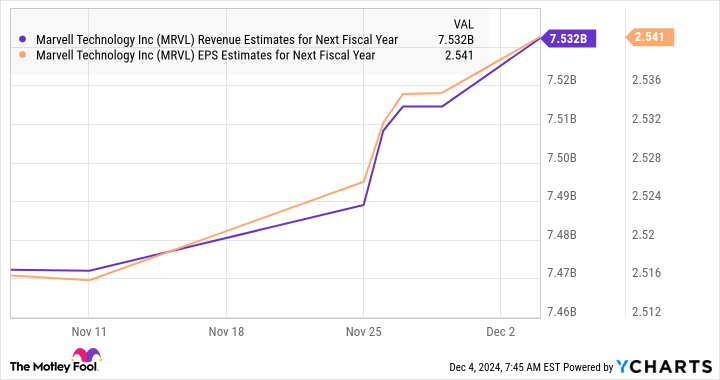

MRVL Revenue Estimates for Next Fiscal Year data by YCharts

The top-line forecast for fiscal 2026 points toward a 31% increase, while the bottom line will increase by an impressive 63%. Of course, it won’t be surprising to see analysts bumping up their estimates following Marvell’s latest quarterly report.

However, even if Marvell manages to achieve $7.5 billion in sales next year and trades at 16 times sales at that time, its market capitalization could hit $120 billion. That would be a 43% increase from current levels. However, the market has rewarded the likes of Nvidia with a much higher sales multiple of 31.

If something similar happens with Marvell and the company manages to deliver stronger growth in 2025, it may be able to deliver much stronger gains than what’s projected above.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $376,143!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,028!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $494,999!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of December 2, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool recommends Broadcom and Marvell Technology. The Motley Fool has a disclosure policy.

Missed Out on Nvidia? Buy This Magnificent Artificial Intelligence (AI) Stock Before It Soars at Least 43% in 2025. was originally published by The Motley Fool

Dena Holloway is a writer, editor, and content creator based in the United States. She has written for a variety of publications, including Men With Wings Press, where she covers arts, automotive, travel, and fashion. She's also a certified yoga instructor and works as a freelance copywriter.