Medtronic’s revenue growth has been relatively unimpressive in recent years.

The company’s entrance into the robotic-assisted surgery market could help change that.

There are other reasons to invest in Medtronic, including its rock-solid dividend program.

Medical device specialist Medtronic(NYSE: MDT) has not performed well over the past five years; the stock has significantly lagged broader equities. One of the issues it’s encountered is slow revenue growth. Although it explored plans to spin off some of its low-growth units to improve on that front, it eventually abandoned the idea.

However, new developments suggest that Medtronic could soon tap into a significant long-term opportunity. Let’s look deeper into that and discuss what it means for investors.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Medtronic has been developing its robotic-assisted surgery (RAS) device, the Hugo system, for years. The machine is in use in many countries, but it hasn’t been cleared in the U.S. yet. That’s where Medtronic could make the most money, though, so the company has been testing its Hugo system in the U.S. to support regulatory clearance.

Medtronic recently announced that it has moved one step closer to that goal. It finally submitted an application to the U.S. Food and Drug Administration (FDA) for approval of the Hugo system. That’s after the device met its primary safety and efficacy endpoints in a clinical trial with 137 patients who underwent urologic procedures.

If the FDA puts its stamp of approval on the Hugo system for this indication (urologic procedures), it could be a big deal for Medtronic. As the company pointed out two years ago, only about 5% of surgeries that could be performed robotically actually were. That matters because minimally invasive robotic surgeries have significant advantages over open procedures. The former use tiny, highly maneuverable instruments and cameras that allow specialists to make small incisions and access the organ to be operated on, while providing a high-definition view.

So there’s no need to make large cuts to skin tissue to access the organs directly. Minimally invasive surgeries have significant advantages for patients and hospital systems, including faster recoveries and shorter stays. Yet the market is severely underpenetrated, and that’s with the current volume of worldwide procedures. Also factor in that the world’s population is aging, which will lead to stronger demand for these surgeries in the long run, since seniors have more medical needs; things look good for Medtronic in this market.

True, the company will be entering an industry dominated by Intuitive Surgical, maker of the da Vinci system, a RAS device that has long been cleared for urologic procedures. But considering how open this field is, there should be room for many more players. Medtronic’s Hugo system is currently seeking approval only for urologic procedures, but it will target other therapeutic areas in the future. As the company collects more approvals, the Hugo system should, eventually, make a meaningful impact on its financial results.

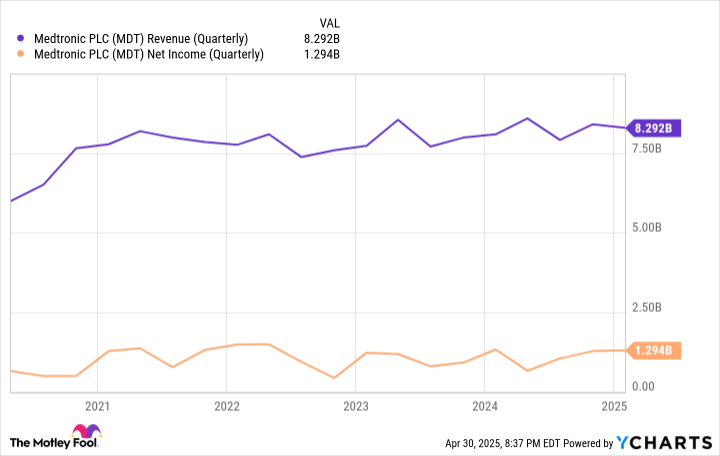

Even though Medtronic’s shares haven’t performed well in recent years, its financial results remain pretty solid. Revenue and earnings are consistent, largely thanks to a deep and diversified portfolio of products.

MDT Revenue (Quarterly) data by YCharts.

Medtronic also earns new clearances pretty regularly. Though most of its segments don’t post particularly impressive sales growth, its diabetes care unit has been an exception. Medtronic markets a range of products through this business, including the innovative MiniMed 780G insulin pump, and there should be ample room for growth here. Medtronic is currently seeking to expand the device’s approval to include people with type 2 diabetes; it’s currently cleared in the U.S. only for those with type 1. Considering that up to 95% of diabetics have the type 2 variety, this would be a meaningful expansion.

The diabetes care unit should continue performing well. The approval of the Hugo system will strengthen the entire business. And even with the threat of tariffs that could affect its costs and bottom line, Medtronic’s financial results should remain relatively stable.

The company also has an excellent dividend profile, having raised its payouts for 47 consecutive years. In just three more years, it will join the prestigious clique of Dividend Kings. That makes Medtronic a top stock for income seekers, and the recent Hugo-related developments only make it more attractive.

Before you buy stock in Medtronic, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Medtronic wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider whenNetflixmade this list on December 17, 2004… if you invested $1,000 at the time of our recommendation,you’d have $623,685!* Or when Nvidiamade this list on April 15, 2005… if you invested $1,000 at the time of our recommendation,you’d have $701,781!*

Now, it’s worth notingStock Advisor’s total average return is906% — a market-crushing outperformance compared to164%for the S&P 500. Don’t miss out on the latest top 10 list, available when you joinStock Advisor.

See the 10 stocks »

*Stock Advisor returns as of April 28, 2025

Prosper Junior Bakiny has positions in Intuitive Surgical. The Motley Fool has positions in and recommends Intuitive Surgical. The Motley Fool recommends Medtronic and recommends the following options: long January 2026 $75 calls on Medtronic and short January 2026 $85 calls on Medtronic. The Motley Fool has a disclosure policy.

This Magnificent High-Yield Dividend Stock Just Became an Even Better Buy was originally published by The Motley Fool